Tackling income tax as a self-employed freelancer or sole trader in the United Kingdom can feel overwhelming without formal accounting training. Misunderstandings about progressive tax rates and the rules for what you actually owe are common, yet these misconceptions can lead to costly errors. By unpacking the basics and demystifying the most persistent myths, this guide highlights income tax fundamentals and shows practical ways to manage your Self Assessment responsibilities with greater confidence.

Table of Contents

- Income Tax Basics And Common Misconceptions

- Types Of Income Tax For The Self-Employed

- How Uk Self Assessment Tax Works

- Legal Responsibilities And Reporting Requirements

- Financial Risks, Penalties, And Frequent Mistakes

Key Takeaways

| Point | Details |

|---|---|

| Understanding Tax Obligations | Self-employed individuals must grasp the complexities of income tax, including progressive rates and different types of taxes applicable to their income. |

| Importance of Record-Keeping | Accurate and comprehensive financial documentation is essential for compliant tax management and to avoid legal penalties. |

| Proactive Tax Management | Developing strategic financial plans and maintaining timely submissions can prevent costly mistakes and potential financial risks. |

| Separate Financial Accounts | Establishing dedicated business bank accounts simplifies income tracking, reduces errors, and enhances overall tax efficiency. |

Income tax basics and common misconceptions

Understanding income tax is crucial for self-employed individuals navigating the complex landscape of tax obligations. The fundamental principle is straightforward: income tax is a mandatory financial contribution levied on personal earnings by governmental authorities. However, many self-employed workers misunderstand its core mechanisms and implications.

There are several key misconceptions about income tax that can lead to costly mistakes:

- Believing all income is taxed equally: Tax systems typically employ progressive rates where higher earnings attract higher tax percentages

- Assuming tax calculations are simple: Self-employed individuals must track multiple income streams and allowable expenses

- Thinking tax avoidance is legal: There’s a significant difference between legitimate tax planning and illegal tax evasion

- Overlooking national insurance contributions: These are often interconnected with income tax obligations for self-employed workers

The progressive nature of tax systems means that tax rates increase as your income rises, creating a graduated system where different income brackets are taxed at varying percentages. This complexity underscores why self-employed professionals must maintain meticulous financial records and understand their specific tax responsibilities.

Accurate record-keeping is not optional – it’s essential for compliant and stress-free tax management.

Self-employed individuals must recognise that their tax responsibilities extend beyond simple income reporting. They need to consider factors like:

- Tracking all business and personal income sources

- Calculating allowable business expenses

- Understanding tax relief and deduction opportunities

- Maintaining comprehensive financial documentation

Professional tax management requires more than basic arithmetic. It demands strategic financial planning, consistent documentation, and a proactive approach to understanding evolving tax regulations.

Pro tip: Create a dedicated business bank account to simplify income tracking and separate personal and professional finances, making tax preparation significantly easier.

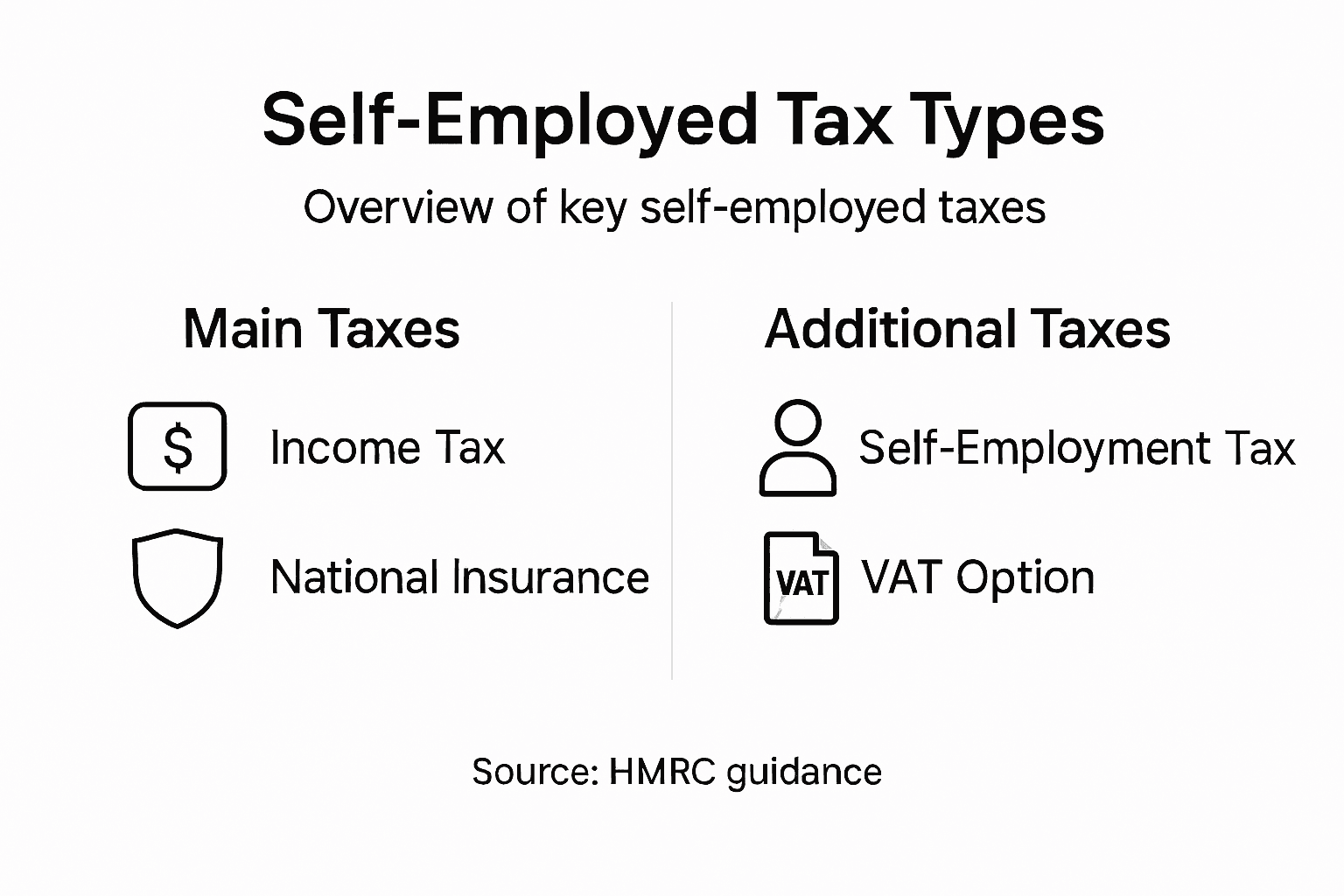

Types of income tax for the self-employed

Self-employed individuals face a unique and complex tax landscape that extends beyond traditional employment taxation. Understanding the various types of income tax is crucial for maintaining financial compliance and minimising unexpected tax burdens. These tax obligations can significantly impact a freelancer’s or sole trader’s overall financial strategy.

The primary types of income tax for self-employed professionals include:

- Self-Employment Tax: A mandatory contribution covering Social Security and Medicare responsibilities

- Income Tax: Annual tax on total earnings from business and personal sources

- National Insurance Contributions: Mandatory payments that support state benefits and pension systems

- Class 2 and Class 4 National Insurance: Specific categories of tax for self-employed individuals

Self-employment tax fundamentals reveal a comprehensive tax structure where self-employed workers must cover both employer and employee tax contributions. This typically amounts to a 15.3% total tax rate, which includes 12.4% for Social Security and 2.9% for Medicare, significantly different from standard employment taxation models.

To clarify the types of taxes self-employed individuals face, see this comparative overview:

| Tax Type | Purpose | Who Pays | Impact on Self-Employed |

|---|---|---|---|

| Income Tax | Annual tax on total personal and business income | All individuals | Major portion of tax owed |

| Self-Employment Tax | Covers National Insurance and social security | Self-employed workers | Full responsibility, not shared |

| National Insurance (Class 2/4) | Funds state pension and benefits | Self-employed (Class 2/4) | Must pay both classes if eligible |

Self-employed professionals must proactively manage their tax responsibilities to avoid potential financial penalties.

The tax system recognises multiple income streams for self-employed individuals, including:

- Profits from sole trading activities

- Income from freelance contracts

- Earnings from multiple business sources

- Investment and passive income

Understanding these tax classification systems helps self-employed workers develop more sophisticated financial planning strategies. Each income type may be subject to different tax rates and reporting requirements.

Professional tax management demands meticulous record-keeping, understanding of complex tax regulations, and strategic financial planning to optimise tax efficiency.

Pro tip: Maintain separate bank accounts for personal and business finances to simplify tax reporting and reduce the risk of inadvertent tax reporting errors.

How UK Self Assessment tax works

The UK Self Assessment tax system is a crucial mechanism for self-employed individuals to report their annual income and tax liabilities directly to HM Revenue & Customs (HMRC). Unlike traditional employment where taxes are automatically deducted, self-employed professionals must take personal responsibility for calculating and submitting their tax returns accurately and on time.

Key components of the Self Assessment process include:

- Registration: Mandatory for anyone earning over £1,000 through self-employment

- Annual Tax Return: Detailed declaration of income from all sources

- Tax Calculation: Determining total tax owed based on reported earnings

- Payment Deadlines: Specific dates for submitting returns and making tax payments

Self Assessment tax return requirements mandate that individuals register online with HMRC, complete their digital or paper tax return, and submit both the return and any tax owed by specific deadlines. The typical timeline involves registering by 5 October following the end of the tax year, with online submissions due by 31 January.

Timely and accurate reporting is essential to avoid potential penalties and financial complications.

The Self Assessment process involves several critical steps:

- Registering for Self Assessment with HMRC

- Keeping comprehensive financial records

- Calculating total income from all sources

- Completing the online or paper tax return

- Submitting the return and paying any tax owed

Understanding detailed Self Assessment guidelines helps self-employed workers navigate the complex tax reporting landscape. Each step requires careful attention to detail and compliance with HMRC regulations.

Professional tax management demands a proactive approach, combining meticulous record-keeping with a clear understanding of tax obligations and deadlines.

Pro tip: Create a dedicated digital folder to store all financial documents throughout the tax year, making your Self Assessment preparation significantly smoother and less stressful.

Legal responsibilities and reporting requirements

Self-employed individuals in the UK face a complex web of legal responsibilities and reporting requirements that extend far beyond simple income declaration. These obligations are designed to ensure transparent financial reporting, fair taxation, and compliance with HM Revenue & Customs (HMRC) regulations. Understanding and meeting these requirements is not just a legal necessity, but a critical aspect of maintaining a professional and sustainable business.

Key legal responsibilities for self-employed professionals include:

- Accurate Income Reporting: Declaring all business and personal income sources

- Tax Return Submission: Completing Self Assessment returns by specified deadlines

- Record Keeping: Maintaining comprehensive financial documentation for six years

- Tax Payment: Fulfilling tax obligations within prescribed timeframes

- National Insurance Contributions: Making mandatory social security payments

Self-employment tax obligations require meticulous attention to detail, particularly when reporting income and calculating tax liabilities. Professionals must track all earnings, including invoices, contracts, and additional income streams, ensuring complete transparency with tax authorities.

Legal non-compliance can result in significant financial penalties and potential legal consequences.

The reporting process involves several critical documentation requirements:

- Maintaining detailed business income and expense records

- Preserving invoices, receipts, and financial statements

- Tracking bank transactions related to business activities

- Documenting all sources of income

- Preparing accurate financial summaries for tax submissions

Small business tax responsibilities emphasise the importance of comprehensive record-keeping and proactive financial management. Each document serves as evidence of your business’s financial activities and can protect you during potential tax investigations.

Professional compliance requires a systematic approach to financial documentation, combining technological tools with meticulous personal oversight.

Pro tip: Invest in a reliable digital accounting system that automatically categorises and stores financial documents, reducing the administrative burden of tax preparation and ensuring consistent record-keeping.

Financial risks, penalties, and frequent mistakes

Self-employed professionals navigate a treacherous financial landscape where mistakes can lead to substantial penalties and significant financial consequences. Understanding the potential risks and common pitfalls is crucial for maintaining financial stability and avoiding costly errors with HMRC.

Frequent mistakes that can trigger financial risks include:

- Incorrect Income Reporting: Underestimating or misreporting total earnings

- Missing Deadlines: Failing to submit tax returns or make payments on time

- Poor Record-Keeping: Inadequate documentation of business transactions

- Miscalculating Expenses: Claiming inappropriate or unverifiable business expenses

- Overlooking National Insurance Contributions: Neglecting mandatory social security payments

Tax penalties for non-compliance can be severe and multi-layered. HMRC imposes escalating financial sanctions for late submissions, incorrect reporting, and unpaid tax liabilities, with penalties potentially increasing dramatically for repeated or deliberate non-compliance.

Financial penalties can quickly snowball, transforming a minor oversight into a significant financial burden.

The most critical areas of potential financial risk involve:

- Late tax return submissions

- Underpayment of estimated taxes

- Inaccurate income declarations

- Failure to maintain proper financial records

- Missing payment deadlines

Self-employment tax underpayment risks highlight the importance of making accurate estimated tax payments throughout the year. Professionals who miscalculate their tax obligations can face substantial additional charges and interest payments.

Here is a summary of common financial risks and their potential outcomes for self-employed professionals:

| Risk Area | Potential Outcome | Prevention Strategy |

|---|---|---|

| Late Tax Submission | Penalties and interest charges | Set reminders, plan ahead |

| Inaccurate Reporting | Fines, HMRC investigations | Double-check figures, use software |

| Poor Record-Keeping | Difficulty verifying claims, extra scrutiny | Use digital tools, regular review |

| Underpayment of Tax | Additional charges and accumulating debt | Estimate tax, maintain savings |

Financial risk management requires a proactive, systematic approach to tax compliance, combining meticulous documentation with strategic financial planning.

Pro tip: Set calendar reminders for all tax-related deadlines and allocate a separate savings account specifically for tax payments to avoid unexpected financial strain.

Take Control of Your Self-Employment Income Tax with Confidence

Navigating the complexities of income tax can be overwhelming for self-employed professionals who must manage multiple income streams, national insurance contributions and strict reporting deadlines. This article highlights the challenges of accurate income reporting, diligent record-keeping and understanding the UK Self Assessment process — all essential yet demanding tasks that, if mishandled, risk costly penalties and financial stress. If you aim to simplify your tax responsibilities while ensuring full compliance and maximising accuracy, reliable support is within reach with Tax Support – Taxtotal.

Start managing your self-employed tax obligations the smart way at Taxtotal.co.uk. Our platform provides an easy-to-use interface designed specifically for freelancers, sole traders and small business owners who want precise real-time tax calculations, seamless HMRC submission and expert review. Benefit from tools that guide you through income and expenses, reduce errors and keep you on track with deadlines. Don’t wait for penalties to build up — take action now to gain clarity and peace of mind with personalised tax support from Taxtotal.co.uk. Learn more and get started today by visiting https://taxtotal.co.uk.

Frequently Asked Questions

What are the common misconceptions about income tax for the self-employed?

Many self-employed individuals believe all income is taxed equally, assume tax calculations are straightforward, think tax avoidance is legal, and overlook national insurance contributions. Understanding these misconceptions can help avoid costly mistakes.

How does the UK Self Assessment tax system work for self-employed individuals?

The UK Self Assessment tax system requires self-employed individuals to report their annual income directly to HMRC, calculate their tax liabilities, and submit tax returns by specified deadlines. Unlike traditional employment, taxes are not automatically deducted from earnings.

What types of income tax do self-employed professionals need to pay?

Self-employed individuals are typically responsible for self-employment tax, income tax on total earnings, and national insurance contributions, including Class 2 and Class 4 payments, which fund benefits and pensions.

What are the potential penalties for non-compliance with income tax reporting?

Penalties can arise from incorrect income reporting, missed deadlines, poor record-keeping, and underpayment of taxes. These penalties can significantly increase for repeated offences or deliberate non-compliance.