Missing the Self Assessment deadline with HM Revenue and Customs can cost you £100 instantly, even if you owe no tax. Freelancers and sole traders across the United Kingdom face the unique challenge of reporting income that does not have tax deducted automatically. Understanding the process is vital to avoid penalties while keeping your finances in order. This guide breaks down what matters most, from registration to deadlines and the steps to file accurately, so you can confidently manage your Self Assessment each year.

Table of Contents

- Self Assessment Tax Explained For The UK

- Who Must File And Common Misconceptions

- The Self Assessment Process Step By Step

- Key Deadlines, Risks, And Penalties

- How To Avoid Mistakes And Simplify Filing

Key Takeaways

| Point | Details |

|---|---|

| Self Assessment Necessity | If you’re self-employed or have untaxed income over £1,000, you must file a Self Assessment tax return. |

| Critical Deadlines | Missing deadlines can result in substantial penalties, so it’s vital to be aware of key dates, including 5 October, 31 October, and 31 January. |

| Record Keeping Requirements | Maintain accurate records for at least six years as HMRC requires documentation of all income and expenses to substantiate your tax return. |

| Implications of Non-compliance | Failing to file or inaccurately reporting can lead to severe penalties and interest on unpaid tax, making awareness of your obligations crucial. |

Self Assessment Tax Explained for the UK

Self Assessment is how HM Revenue and Customs (HMRC) collects Income Tax from people with income that doesn’t have tax automatically deducted. If you’re a freelancer or sole trader, you’ll almost certainly need to file a Self Assessment return each year.

Why Freelancers Need Self Assessment

Unlike employees, your income doesn’t have tax removed automatically from payments you receive. You’re responsible for telling HMRC what you’ve earned and what tax you owe.

You’ll need to register for Self Assessment if:

- You’re self-employed and earn £1,000 or more

- You have income from rental properties

- You have other untaxed income beyond your primary earnings

- HMRC sends you a notice to file

Registration is straightforward and must be completed by specific deadlines or you could face penalties.

Self Assessment isn’t optional if you meet the criteria—it’s a legal requirement. Missing deadlines can cost you hundreds in penalties.

How Self Assessment Works

The process requires you to report all income and expenses through an annual tax return. You’ll calculate your profit, claim allowable expenses, and identify any tax you owe.

Your return covers:

- Self-employment income (turnover minus allowable expenses)

- Capital Gains Tax on asset sales

- Savings interest and dividends

- Any other taxable income

Once filed, HMRC calculates your final tax bill based on your income and the current tax bands. Some people receive refunds; others owe money.

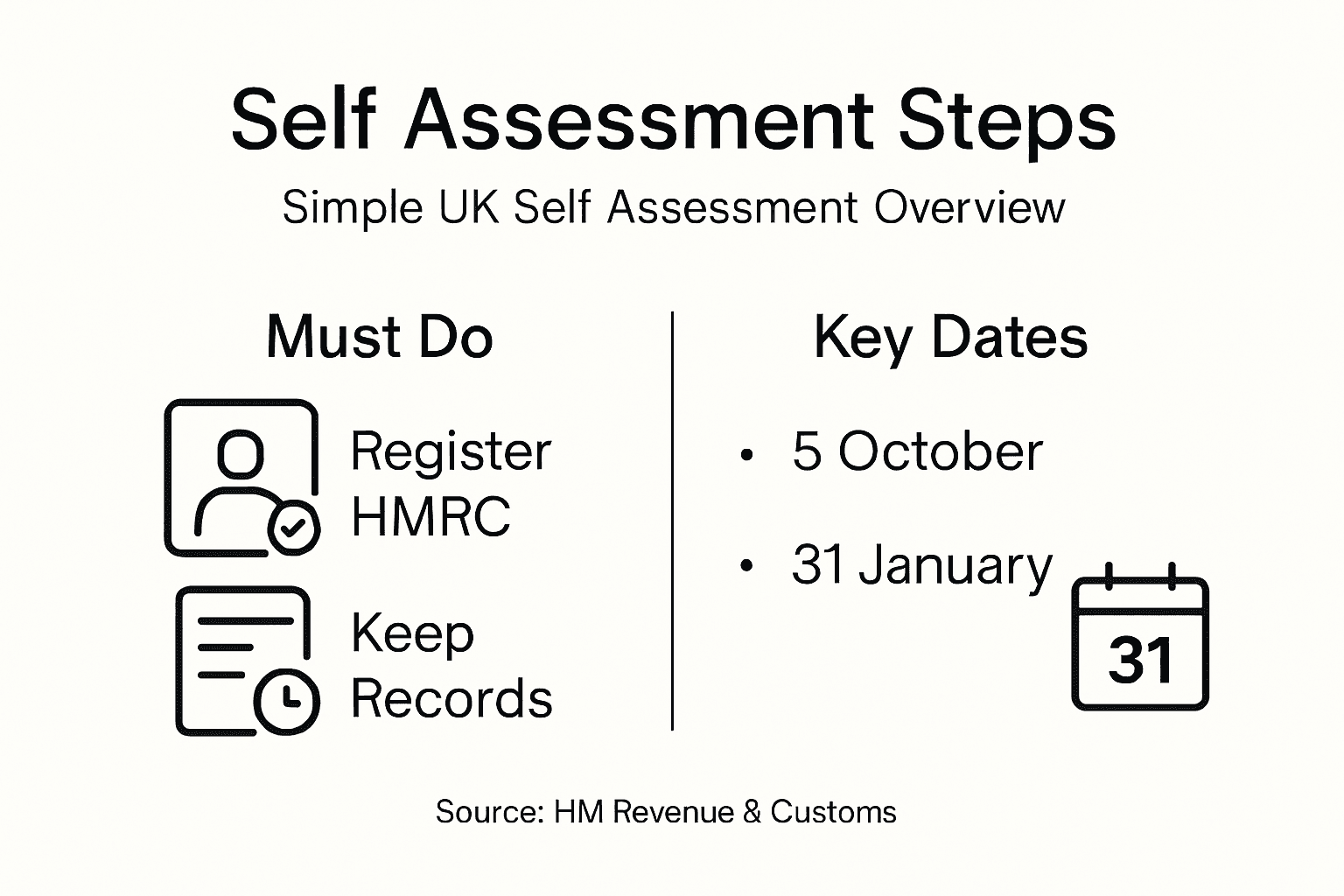

Key Deadlines You Can’t Miss

Missing Self Assessment deadlines triggers automatic penalties. The main dates are:

- Notification deadline: Notify HMRC by 5 October the year after you start self-employment

- Tax return deadline: File your return by 31 January following the end of the tax year (5 April)

- Payment deadline: Pay your tax bill by 31 January

File even one day late and you’ll automatically receive a £100 penalty, regardless of whether you owe tax.

What Information You Need

Gather these essentials before you sit down to complete your return:

- Total income earned during the tax year (invoices, contracts, client statements)

- Business expenses (receipts, invoices, bank statements)

- Capital gains (if you sold assets)

- Interest earned from savings

- Any other untaxed income sources

Keeping good records throughout the year makes this process far less stressful when it comes to filing.

Keeping accurate records isn’t just recommended—HMRC requires you to keep them for at least six years.

Why It Matters to You

Self Assessment determines how much tax you actually owe, whether you’re entitled to refunds, and what penalties apply if you don’t file on time. Getting it wrong can be expensive; getting it right protects your business.

Pro tip: Set aside a percentage of your income weekly (typically 20-25%) to cover your tax bill, so you’re not scrambling to find the money when January rolls around.

Who Must File and Common Misconceptions

Not everyone needs to file a Self Assessment tax return, but the rules are broader than many people think. Understanding who must file prevents costly mistakes and helps you stay compliant with HMRC requirements.

Who Actually Needs to File

You must file a Self Assessment tax return if you were self-employed and earned more than £1,000 before expenses during the tax year. This threshold applies even if you made minimal profit or a loss.

You’ll also need to file if:

- You’re a partner in a business partnership

- You earned rental income from properties

- You received tips, commissions, or bonuses not taxed through PAYE

- You made capital gains (profit from selling assets)

- You have savings interest or dividend income above your personal savings allowance

- You received foreign income

- You were charged the High Income Child Benefit Charge

Many freelancers assume they’re the only ones who file, but rental income, investment returns, and secondary earnings all trigger the requirement.

Common Misconception #1: “I Only File If Self-Employed”

This is false. You can be employed full-time, earning a salary through PAYE, and still need to file if you have other income sources. A second income stream—whether it’s freelance work, rental property, or investment returns—can trigger the requirement to file.

Even small amounts matter. If you earn £50 from tutoring alongside your job, you may need to file depending on your circumstances.

Self Assessment isn’t exclusively for the self-employed; it applies whenever you have untaxed or complex income.

Common Misconception #2: “My Income Is Too Low to Matter”

The £1,000 threshold is important, but HMRC doesn’t care if you think you owe nothing. Filing is about reporting accurately, regardless of the amount. Missing a return you should have filed means automatic penalties, even if you owed zero tax.

You can check if you need to file using HMRC’s online tool if you’re uncertain about your situation. It takes a few minutes and removes the guesswork.

Common Misconception #3: “HMRC Will Contact Me If I Owe Tax”

HMRC won’t chase you if you haven’t filed. In fact, if you should have filed and didn’t, you’re breaking the law. You’re responsible for knowing whether you need to file and for meeting the deadline.

The onus is entirely on you. HMRC expects self-assessment to be self-initiated.

Who Doesn’t Need to File

If you’re employed, pay tax through PAYE, and have no other income or complex circumstances, you probably don’t need to file. Basic employees with straightforward tax situations don’t require Self Assessment.

But if there’s any doubt, check. Getting it wrong is more costly than filing when you weren’t strictly required to.

To clarify who must file a Self Assessment return, see the common scenarios compared below:

| Situation | Must File? | Reason |

|---|---|---|

| Sole trader earning £1,500 | Yes | Self-employment income exceeds £1,000 threshold |

| Employed, no side income | No | PAYE covers all earnings, no extra sources |

| Rental income £2,000/year | Yes | Untaxed property income triggers filing requirement |

| £60 interest from savings | Possibly | Depends if above personal savings allowance |

| Employed and £50 freelance work | Possibly | Must check total untaxed income and thresholds |

When in doubt, file. The cost of an unnecessary return is far less than the penalty for missing a required one.

Pro tip: Use HMRC’s online checker before the 5 October notification deadline to confirm your filing status—it’s free and takes minutes, saving you months of uncertainty.

The Self Assessment Process Step by Step

The Self Assessment process might seem daunting, but breaking it down into manageable steps makes it straightforward. You’ll move through registration, data gathering, completing your return, and payment in a logical sequence.

Step 1: Check If You Need to File

Before doing anything else, confirm that you actually need to file. Review the criteria from earlier—self-employment income, rental earnings, investment returns, and other untaxed income all trigger the requirement.

If you’re uncertain, use HMRC’s online checker or contact their helpline. This five-minute step prevents months of unnecessary work.

Step 2: Register for Self Assessment

Once you’ve confirmed you need to file, you must register with HMRC to obtain a Unique Taxpayer Reference. Registration must happen by 5 October following the tax year in which you became self-employed or met the filing criteria.

Your UTR is essential—you’ll need it for all future Self Assessment filings and communications with HMRC. Registration typically takes a few days.

Step 3: Gather Your Financial Records

Collect everything before you sit down to file. This includes:

- Bank statements and invoices showing all income

- Receipts for business expenses

- Records of capital gains (asset sales)

- Savings interest statements

- Dividend statements from investments

- Payslips if you have employment income

Organising records as you go throughout the year saves enormous time come filing season. Many freelancers store receipts digitally or use bookkeeping software.

Accurate records aren’t optional—HMRC requires you keep them for six years, and they’re your defence if audited.

Step 4: Complete Your Tax Return

You can file online or on paper. Online filing is simpler, faster, and safer; HMRC encourages it and gives you until 31 January. Paper returns must arrive by 31 October, giving you less time.

Your return includes:

- Your income from all sources

- Allowable business expenses

- Any reliefs or allowances you’re entitled to claim

- Capital gains information

- Tax calculations (HMRC’s software does this automatically)

Review everything carefully before submitting—errors now cost time later.

Step 5: Submit Your Return

Hit submit by the deadline. Online filing closes at midnight on 31 January. HMRC sends instant confirmation once received.

You can amend your return within 12 months of the filing deadline if you discover mistakes. Report errors promptly to avoid penalties.

Step 6: Pay Your Tax Bill

Any tax owed must be paid by 31 January. HMRC issues a statement showing what you owe after they’ve processed your return.

Missing the payment deadline triggers interest and penalties on top of your bill. Set up a standing order or mark your calendar weeks in advance.

Paying on time protects your credit file and prevents costly interest charges.

Pro tip: Complete your return several weeks before the deadline so you have time to fix any errors HMRC queries and arrange payment without rushing.

Key Deadlines, Risks, and Penalties

Missing Self Assessment deadlines isn’t a minor inconvenience—it triggers automatic penalties that accumulate quickly. Understanding the dates and consequences protects your finances and reputation.

Critical Deadlines You Cannot Miss

Three deadlines matter most. First, notify HMRC by 5 October if you need to file a return. Second, submit paper returns by 31 October. Third, file online and pay any tax owed by 31 January following the end of the tax year.

If you have a second payment on account (quarterly instalments), that’s due 31 July. Missing any of these triggers penalties immediately.

Here is a summary comparing key Self Assessment deadlines and the impact of missing them:

| Deadline Type | Due Date | What Happens If Missed | Penalty Amount |

|---|---|---|---|

| Notification to HMRC | 5 October | May need to file late, triggers fines | Possible £100+ fine |

| Paper return submission | 31 October | Must file online instead if missed | Online deadline then applies |

| Online return & payment | 31 January | Immediate fixed fine added | £100 at minimum |

| Second payment (if due) | 31 July | Interest and additional penalty | 5% of unpaid tax |

What Happens When You Miss a Deadline

The penalties are harsh and escalate quickly. Miss the filing deadline by even one day and you receive an immediate £100 fixed penalty—regardless of whether you owe tax.

After three months without filing, HMRC charges £10 per day up to a maximum of £900. At six months, you face a penalty of either £300 or 5% of the tax owed (whichever is higher). At 12 months, it increases to £600 or 5% of tax owed.

These penalties stack on top of your actual tax bill.

One missed deadline costs £100 minimum. Two years of missed deadlines could cost thousands in penalties alone.

Late Payment Penalties and Interest

Paying tax late triggers interest charges on top of your bill. Interest accrues daily from the payment deadline until you settle the full amount.

You’ll also face a 5% penalty if payment is more than 30 days late, another 5% at six months, and a further 5% at 12 months. These compound, making late payment expensive fast.

Penalties for Inaccurate Returns

Submitting a return with errors or deliberately understating income brings additional penalties. Careless mistakes incur 30% penalties. Deliberate understatement can result in 70% penalties plus prosecution.

Even honest errors cost money if discovered during an HMRC review.

What Gives You a Defence

HMRC may waive penalties if you have a reasonable excuse for missing the deadline. Examples include serious illness, bereavement, or a genuine professional error beyond your control.

Simple excuses like “I forgot” or “I was busy” don’t qualify. Document any genuine issues immediately if they apply to you.

Can You Get Extra Time?

You cannot extend the filing deadline, but HMRC allows flexible payment arrangements. If you cannot pay by 31 January, contact HMRC immediately to arrange a payment plan.

Paying late incurs interest, but a plan prevents the escalating penalties that non-payers face.

Contact HMRC before the deadline if you cannot pay—waiting until after costs far more.

Pro tip: Set calendar reminders for 31 December and 31 January so you cannot accidentally miss deadlines; many freelancers use their accountant’s email alerts as a backup.

How to Avoid Mistakes and Simplify Filing

Most filing errors stem from poor organisation and rushing at the last minute. Building good habits throughout the year transforms Self Assessment from stressful to straightforward.

Start Early and Stay Organised

Register for Self Assessment as soon as you know you need to file. Early registration gives you your Unique Taxpayer Reference in time and removes that task from your to-do list.

Throughout the year, keep a dedicated folder for receipts, invoices, and bank statements. Digital storage via cloud services or bookkeeping software beats shoebox accounting every time.

Gather Everything Before You Start

Collect all documents you’ll need before opening your return. This prevents mid-filing panic when you realise you’re missing information.

You’ll need:

- Bank statements showing all deposits

- Invoices sent to clients

- Receipts for every business expense

- P60 forms if you had employment income

- Property income records if applicable

- Capital gains documentation

- Pension contribution statements

Organising by month or category makes data entry faster and more accurate.

Gathering documents first cuts filing time in half and reduces errors significantly.

File Online, Not on Paper

Online filing is faster, safer, and gives you until 31 January rather than 31 October. The system catches obvious errors immediately and calculates your tax automatically.

Paper forms require manual maths, take longer to process, and offer no error checking. If you can access a computer, file online.

Break It Into Stages

Don’t attempt your entire return in one sitting. Complete it in sections over several days.

Start with self-employment income, then move to other income sources. Add expenses next, then reliefs and allowances. Leave review and submission for the final stage.

This approach reduces errors because you’re focused on one area at a time.

Use HMRC Resources

HMRC provides detailed helpsheets and video tutorials for every section of your return. These are free and specifically written for Self Assessment filers.

Webinars and email support also help with tricky questions. Using official resources prevents misunderstandings about what to include or claim.

Double-Check Before Submitting

Review your return carefully. Check that income figures match your records, expenses are reasonable, and all sections are complete.

A five-minute review saves hours of corrections later.

Mistakes after submission cost time and stress—spending 15 minutes reviewing prevents both.

Pro tip: Complete your return by mid-January rather than waiting until the deadline, giving you time to fix errors and arrange payment without panic.

Simplify Your Self Assessment Tax Filing Today

Managing Self Assessment tax can feel overwhelming with strict deadlines, complex income sources, and the constant risk of costly penalties. If you are a freelancer or sole trader trying to navigate untaxed income, allowable expenses, or the fear of late filing fines, you are not alone. Understanding exactly what to report, when to file, and how much tax you owe is crucial but can be stressful without clear guidance or the right tools.

Take control now with Taxtotal.co.uk. Our easy-to-use platform is designed specifically for UK self-employed individuals like you. It helps you prepare, review, and submit your Self Assessment tax return accurately and on time, all from one place. Benefit from real-time tax calculations, automatic error checks, and expert support to reduce stress and avoid penalties. Visit Taxtotal.co.uk to start simplifying your tax journey today and ensure compliance is never a worry again. For more details on registration and filing, explore our How to Register for Self Assessment with HMRC guide and get ready to file with confidence.

Frequently Asked Questions

What is Self Assessment tax?

Self Assessment tax is the system HM Revenue and Customs (HMRC) uses to collect Income Tax from individuals who do not have tax automatically deducted from their earnings, typically self-employed individuals, freelancers, and those with additional untaxed income.

Why do freelancers need to file a Self Assessment tax return?

Freelancers need to file a Self Assessment tax return because their income does not have tax deducted at source. They are responsible for reporting their earnings to HMRC and calculating the tax they owe based on their total income and allowable expenses.

What are the key deadlines for Self Assessment tax filing?

The key deadlines include: notify HMRC by 5 October if you need to file, submit paper returns by 31 October, and file online and pay any tax owed by 31 January following the end of the tax year.

What happens if I miss a Self Assessment deadline?

Missing a Self Assessment deadline can lead to automatic penalties. For instance, an immediate £100 fine is charged if you file one day late, and further penalties accrue if delays continue. It’s crucial to meet all deadlines to avoid excessive fees.