Keeping your business finances organised as a sole trader in the United Kingdom can feel like a constant juggling act, especially when Self Assessment deadlines approach. Efficient bookkeeping not only takes the pressure off your tax return but also helps you see exactly where every pound goes. This straightforward guide reveals simple steps and the most suitable tools to help you maintain clear, compliant, and organised financial records from day one.

Table of Contents

- Step 1: Set Up Essential Bookkeeping Tools And Records

- Step 2: Organise Income And Expense Sources Efficiently

- Step 3: Track Payments And Manage Invoices Regularly

- Step 4: Reconcile Accounts And Check For Accuracy

- Step 5: Prepare Records For Seamless Self Assessment Filing

Quick Summary

| Key Takeaway | Guidance on Implementation |

|---|---|

| 1. Set up a structured bookkeeping system | Choose suitable recordkeeping tools like digital accounting software to track income and expenses efficiently. |

| 2. Organise income and expenses effectively | Create separate categories for income streams and tax-deductible expenses to ensure comprehensive tracking. |

| 3. Implement consistent payment tracking | Regularly update invoices and track payments to maintain timely cash flow and avoid overdue accounts. |

| 4. Regularly reconcile accounts | Conduct monthly reconciliations to ensure the accuracy of financial records and identify discrepancies swiftly. |

| 5. Prepare documents for Self Assessment | Organise and categorise all financial documents in advance of tax filing, ensuring readiness for potential audits. |

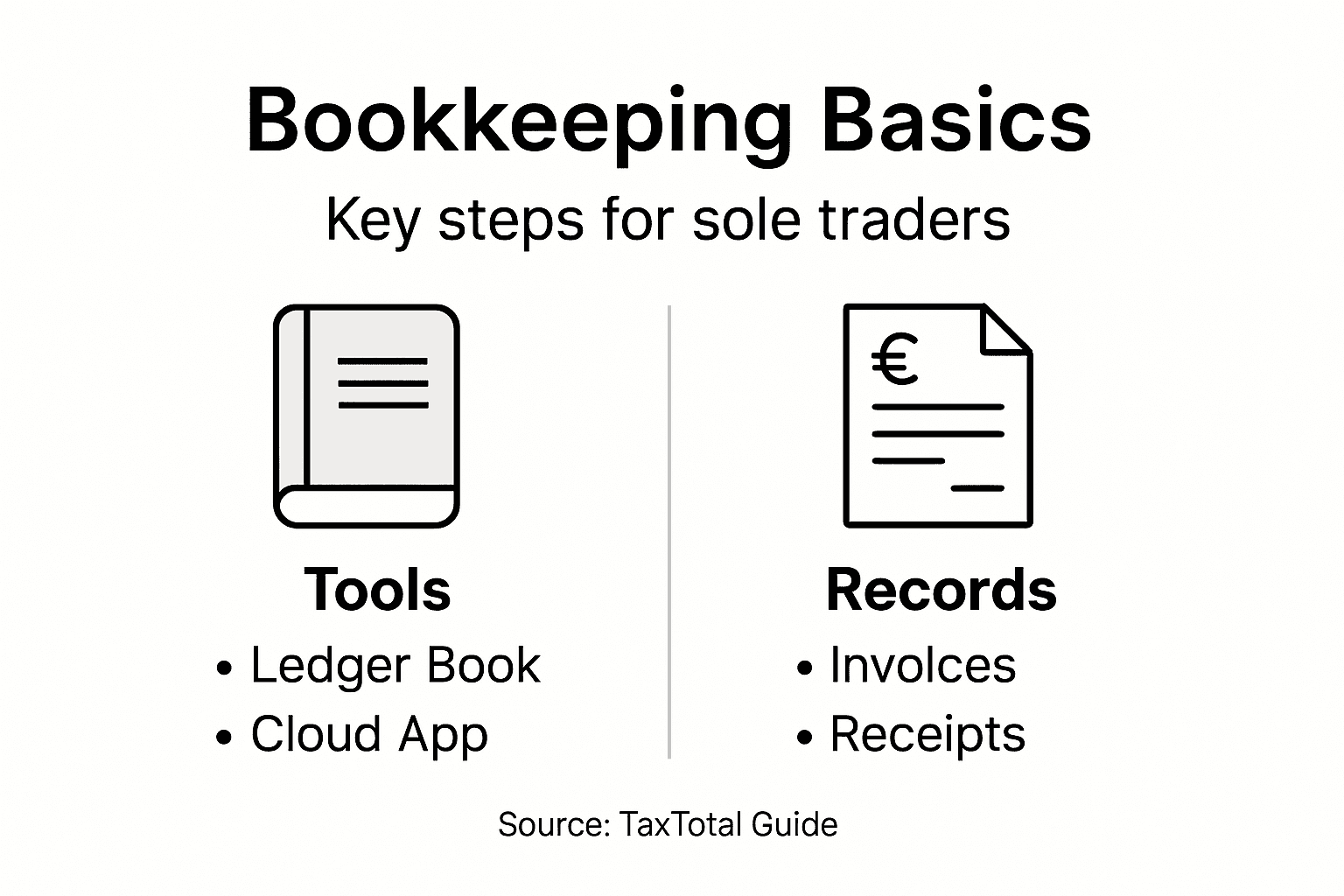

Step 1: Set up essential bookkeeping tools and records

Setting up robust bookkeeping systems is fundamental for smooth financial management and stress-free tax filing as a sole trader. Your goal is creating an organised approach that tracks every pound earned and spent while maintaining clear, compliant financial records.

Start by selecting appropriate recordkeeping tools and methods that match your business complexity. Most sole traders find digital accounting software the most efficient option, though some still prefer traditional ledger books. Your chosen system should enable easy tracking of:

- Income records: Invoices, payment receipts, bank statements

- Expense documentation: Receipts, supplier invoices, transaction logs

- Business asset records: Equipment purchases, depreciation details

- Client and customer information: Contact details, transaction histories

When establishing your bookkeeping framework, choose between cash or accrual accounting methods. The cash method records transactions when money actually changes hands, while accrual accounting logs transactions when they’re invoiced, regardless of payment timing. Most small businesses prefer the straightforward cash method for its simplicity.

Here is a comparison of cash and accrual accounting methods for sole traders:

| Aspect | Cash Method | Accrual Method |

|---|---|---|

| Timing of Recording | When payment is received or made | When invoice is issued or bill received |

| Complexity | Simpler to manage | Requires more detailed tracking |

| Cash Flow Visibility | Provides real-time cash position | May show income before cash arrives |

| Suitability | Ideal for small and straightforward businesses | Suits larger or more complex operations |

| HMRC Acceptance | Accepted for most sole traders | Required for some larger businesses |

Ensure you maintain physical or digital copies of all financial documents for at least six years, as HMRC requires comprehensive record-keeping for potential tax inspections. Scanning and storing documents electronically can provide both convenience and secure backup.

Top tip: Consider using cloud-based accounting software that automatically categorises transactions and generates reports, saving you significant time during tax preparation.

Step 2: Organise income and expense sources efficiently

Organising your income and expense sources systematically is crucial for maintaining clean financial records and simplifying your tax preparation process. Your primary objective is to create a clear, trackable system that captures every financial transaction with precision and clarity.

To achieve this, you’ll want to develop a comprehensive recordkeeping strategy that breaks down your financial activities into distinct, manageable categories. Most successful sole traders implement a structured approach that includes:

- Income tracking: Separate income streams by client, project, or service type

- Expense categorisation: Group expenses into standard tax-deductible categories

- Digital documentation: Create digital copies of all financial documents

- Regular reconciliation: Match bank statements with your financial records monthly

Start by establishing separate bank accounts for business and personal finances. This simple step prevents transaction mixing and makes tracking far more straightforward. Create digital folders organised by tax year, with subfolders for different document types like invoices, receipts, bank statements, and expense records.

Consider using spreadsheets or accounting software that allows you to tag and categorise transactions automatically. Many modern tools can link directly to your bank account, importing transactions and suggesting appropriate expense categories, which dramatically reduces manual data entry time.

Consistently recording and categorising transactions is more important than perfect accounting – focus on regular, accurate documentation.

Pro tip: Spend 15 minutes each week updating your financial records to prevent overwhelming year-end admin tasks.

Step 3: Track payments and manage invoices regularly

Effective payment tracking and invoice management are fundamental to maintaining healthy financial operations for your sole trader business. Your goal is to create a robust system that ensures timely payments, accurate record-keeping, and smooth cash flow management.

To achieve this, you’ll want to develop consistent transaction recording practices that capture every financial interaction with precision. Implementing a systematic approach to invoicing and payment tracking involves several critical strategies:

- Invoice numbering: Create a consistent, sequential numbering system for all invoices

- Payment terms: Clearly define payment deadlines on each invoice (e.g., net 30 days)

- Tracking mechanisms: Use spreadsheets or accounting software to monitor outstanding payments

- Follow-up protocols: Establish a standard process for chasing late payments

Consider using digital invoicing tools that automatically track payment status and send reminders to clients. These platforms can significantly reduce the administrative burden of manual follow-ups and help maintain a professional approach to financial management.

Consistent and prompt invoicing is the backbone of healthy cash flow for sole traders.

Implement a monthly reconciliation process where you compare your issued invoices against received payments. This practice helps identify any discrepancies early and ensures you’re capturing all income accurately for tax reporting purposes.

Pro tip: Set up automatic payment reminders and dedicate a specific day each month to chase and record outstanding invoices to maintain financial discipline.

Step 4: Reconcile accounts and check for accuracy

Account reconciliation is a critical process that ensures your financial records remain precise and trustworthy. Your primary goal is to validate every financial transaction, identifying and resolving any discrepancies before they become complex issues.

To maintain impeccable financial accuracy, you’ll want to implement systematic account reconciliation practices that methodically compare your financial documents. This process involves several strategic steps:

- Bank statement review: Compare bank statements against your personal accounting records

- Transaction matching: Verify each transaction’s amount, date, and description

- Discrepancy investigation: Flag and research any unexplained differences

- Documentation preservation: Keep detailed records of reconciliation processes

Digital accounting tools can significantly streamline this process, automatically highlighting potential inconsistencies and reducing manual checking time. Most modern software platforms offer bank feed integration, which allows real-time transaction importing and simplified reconciliation.

Consistent and thorough account reconciliation prevents potential tax complications and provides clear financial visibility.

Establish a monthly reconciliation routine, ideally selecting a consistent date each month. This regularity helps you catch errors quickly and maintains an up-to-date understanding of your business’s financial health.

Below is a summary of key monthly reconciliation steps to keep your accounts accurate:

| Step | Purpose | Recommended Tool |

|---|---|---|

| Bank statement comparison | Identify differences in records | Online banking, spreadsheets |

| Transaction cross-checking | Ensure every entry is in both ledgers | Digital accounting software |

| Discrepancy investigation and resolution | Resolve errors before filing taxes | Spreadsheet, notes |

| Document reconciliation review | Provide evidence for future inspections | Cloud storage, physical files |

Pro tip: Schedule your reconciliation during a quiet period and create a dedicated spreadsheet template to track and document your review process efficiently.

Step 5: Prepare records for seamless Self Assessment filing

Preparing your financial records for Self Assessment requires a systematic and organised approach that ensures accuracy and compliance. Your goal is to compile and structure your documentation in a manner that makes tax filing straightforward and stress-free.

To achieve this, you’ll want to maintain comprehensive and organised records that support every aspect of your tax return. This preparation involves several critical components:

- Income documentation: Gather all invoices, payment receipts, and bank statements

- Expense categorisation: Collect and sort receipts into standard tax-deductible categories

- Supporting paperwork: Compile contracts, work agreements, and financial correspondence

- Digital organisation: Create a clear, logical folder structure for each tax year

Develop a consistent filing system that allows you to quickly locate any document during your Self Assessment preparation. Consider creating both digital and physical backups of your financial records, ensuring you have multiple layers of documentation protection.

A well-organised record system is your best defence against potential tax inquiries and audits.

Allocate dedicated time in the weeks leading up to the tax return deadline to review and cross-check your documents. This proactive approach helps identify any missing information or potential discrepancies before submitting your Self Assessment.

Pro tip: Create a dedicated tax preparation checklist at the start of each financial year to track and manage your document collection process systematically.

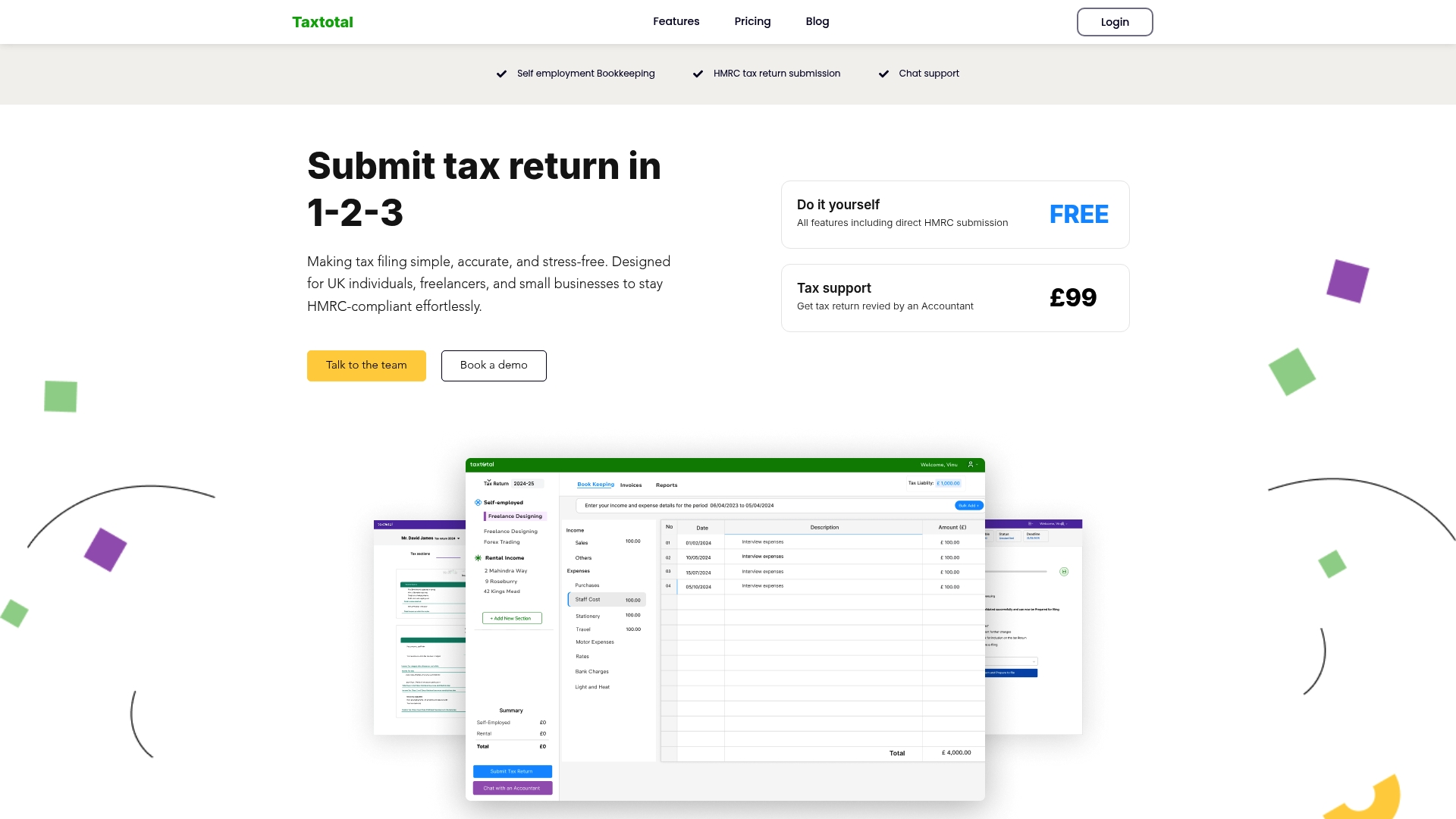

Take Control of Your Sole Trader Bookkeeping with Taxtotal

Managing your bookkeeping for effortless tax filing can feel overwhelming with the need to organise income streams, track expenses, and reconcile accounts accurately. If balancing invoices, payment tracking, and compliance sound familiar, you are not alone. Taxtotal understands these challenges and offers tailored tools to simplify your financial management while ensuring your records are ready for Self Assessment.

Explore our Accounting – Taxtotal resources and benefit from user-friendly software designed for sole traders. Taxtotal’s platform helps you effortlessly categorise expenses, automate invoice tracking, and perform accurate reconciliations. With real-time tax calculations and professional Tax Support – Taxtotal available, you can file confidently and avoid costly mistakes. Start your journey towards stress-free bookkeeping today by visiting Taxtotal.co.uk and gain full control of your self-employment tax management.

Frequently Asked Questions

What essential bookkeeping tools should I use as a sole trader?

To effectively manage your finances, choose bookkeeping tools that suit your business style. Most sole traders benefit from digital accounting software, as it simplifies tracking income, expenses, and assets, while also ensuring compliance with regulations.

How do I categorise my income and expenses for tax purposes?

Organise your financial records by separating income streams and grouping expenses into standard tax-deductible categories. Create digital folders for each tax year, ensuring you can easily locate documents like invoices, receipts, and statements.

What should I do if I notice discrepancies during account reconciliation?

Investigate any discrepancies between your financial records and bank statements promptly. Flag the differences, then cross-check transactions to identify and resolve errors as soon as possible to maintain accuracy in your records.

How can I prepare for Self Assessment filing as a sole trader?

Begin your Self Assessment preparation by gathering all necessary income documentation, expense records, and supporting paperwork. Allocate time in the weeks leading up to the deadline to ensure everything is organised and complete, allowing for a smooth filing process.

How often should I reconcile my accounts?

Aim to reconcile your accounts at least once a month to ensure financial accuracy. Dedicate a specific day each month for this task to catch errors early and keep your financial records up to date and reliable.